Competitive Pricing and Availability Trends of South Africa’s Leading Retailers and Brands in 2023

14th Apr, 2023

By Prashant Dixit

South Africa’s eCommerce market is primed for robust growth in 2023 and beyond, despite the short-term impact of COVID19 over the last few years. According to Statista, the country’s eCommerce market size is $7.2 billion in 2023, with an expected CAGR of 12.5% till 2027. South Africa’s user penetration is already as high as 49.4% and is only set to grow. In essence, there is a massive opportunity for retailers to capitalize on.

For retailers, capturing the lowest priced spot among competitors is often the most certain way to attract and convert online shoppers. Ensuring their products are priced competitively on a consistent basis is key to gaining and maintaining market share in this booming market. This requires South Africa’s online retailers to track and compare the pricing of their products relative to their competitors on an ongoing basis.

For brands, ensuring their pricing and discounting strategies are aligned to market trends are key to gaining market share. In addition, on the backdrop of supply chain challenges globally in the recent past, brands need to ensure high stock availability rates to capitalize on rising consumer demand. In addition, as brands conceptualize and implement a cohesive eCommerce strategy, price parity across all online channels becomes increasingly important.

In this report, we leveraged DataWeave’s proprietary data aggregation and analysis platform to focus our analysis on leading South African retailers and brands and their eCommerce performance across several key dimensions.

Our Research Methodology

Retailers tracked: Takealot, ShopRite, Pick n Pay, Leroy Merlin

Number of SKUs: 40,000+

Number of categories: 190+

A few key categories highlighted: Bath, Food, Home, Spirits

Timeline of analysis: Oct 2022 to March 2023

Key metrics reported:

- Price Increase Opportunity: When a retailer can increase the price of its product by a certain amount while continuing to stay the lowest priced among competitors. This directly helps boost margins.

- Price Decrease Opportunity: When a retailer must decrease the price of its product by a certain amount to gain the lowest price position. This helps gain more sales.

- Action Rate: The share of price improvement opportunities (either price increase or price decrease) actually acted on by the retailer within 15 days of the opportunity presenting itself. For example, an action rate of 25% would mean that for every 100 price improvement opportunities identified, the retailer acted on 25 of them within 15 days.

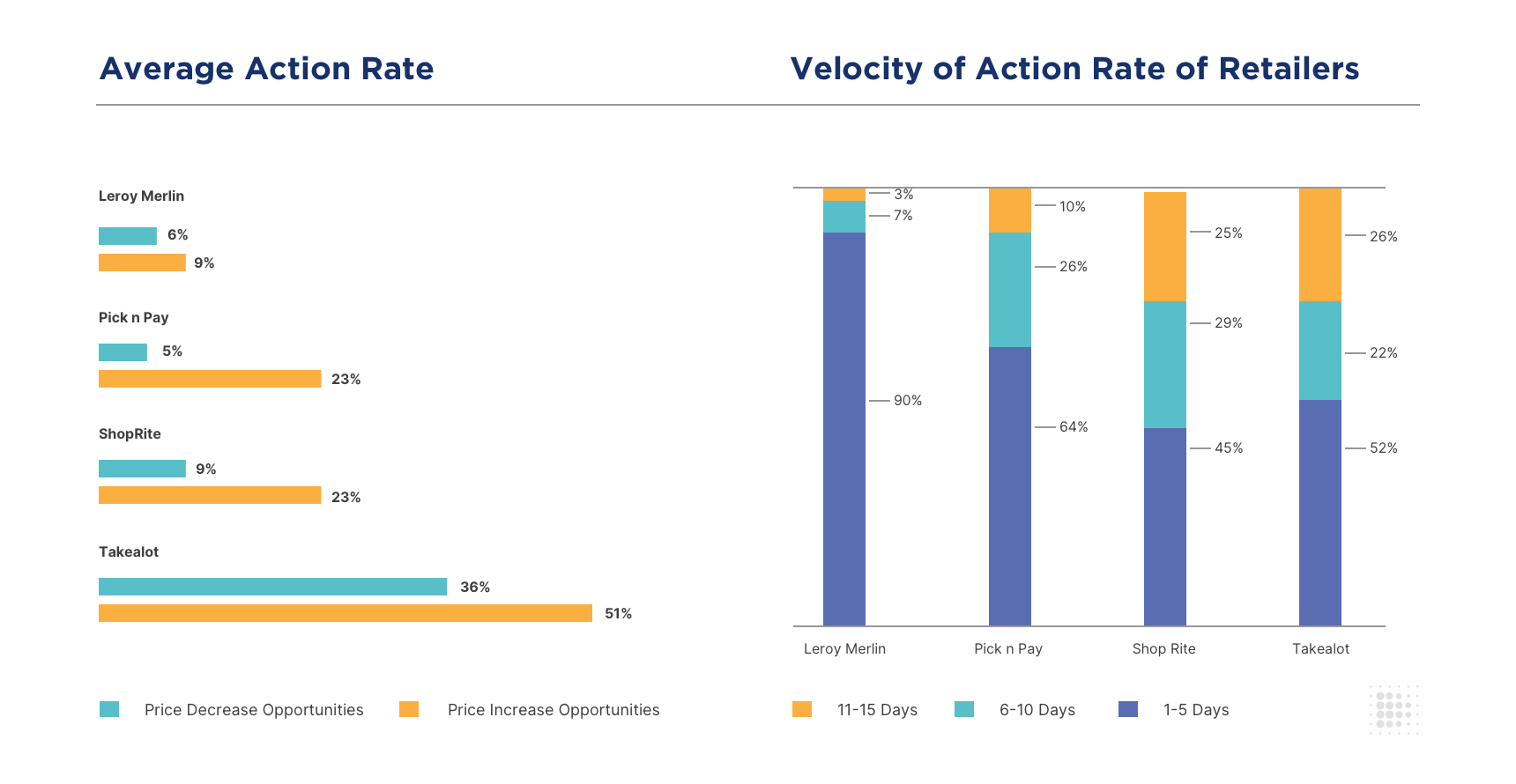

Competitive Pricing Actions of Retailers

Retailers often have dramatically varying approaches to responding to their competitors’ pricing actions. Also, it is not sufficient merely to react but also to react fast. The following chart displays the average action rates for price increase and decrease opportunities, and also breaks down the reported pricing actions into ones acted on within 5 days, 6-10 days, or 11-15 days of the opportunity presenting itself.

Takealot clearly has a strong competitive pricing engine, using which the retailer is able to act on more than half (51%) of price increase opportunities (thereby gaining margin), and over a third (36%) of price decrease opportunities. However, it can do better in acting on many of them faster. Only 52% of the opportunities are acted on within 5 days, while the rest take up to 15 days.

ShopRite and Pick n Pay each have a healthy action rate of 23% for price increase opportunities, but only 9% and 5% respectively on price decrease opportunities. This displays a relatively inconsistent effort in gaining price leadership. ShopRite follows a similar distribution of pricing action velocity as Takealot, albeit for fewer price improvement actions. In comparison to ShopRite, Pick n Pay (which has a similar level of pricing action levels) acts much faster, with 64% of price improvement opportunities acted on within 5 days.

Leroy Merlin acted on only 9% and 6% of its price increase and decrease opportunities, respectively. However, in terms of its velocity of pricing actions, it is far ahead than the rest, with 90% of its pricing actions done within 5 days. This, however, would matter little without strong action rates to begin with. So, Leroy Merlin has a massive opportunity to boost its competitive pricing tracking and operations.

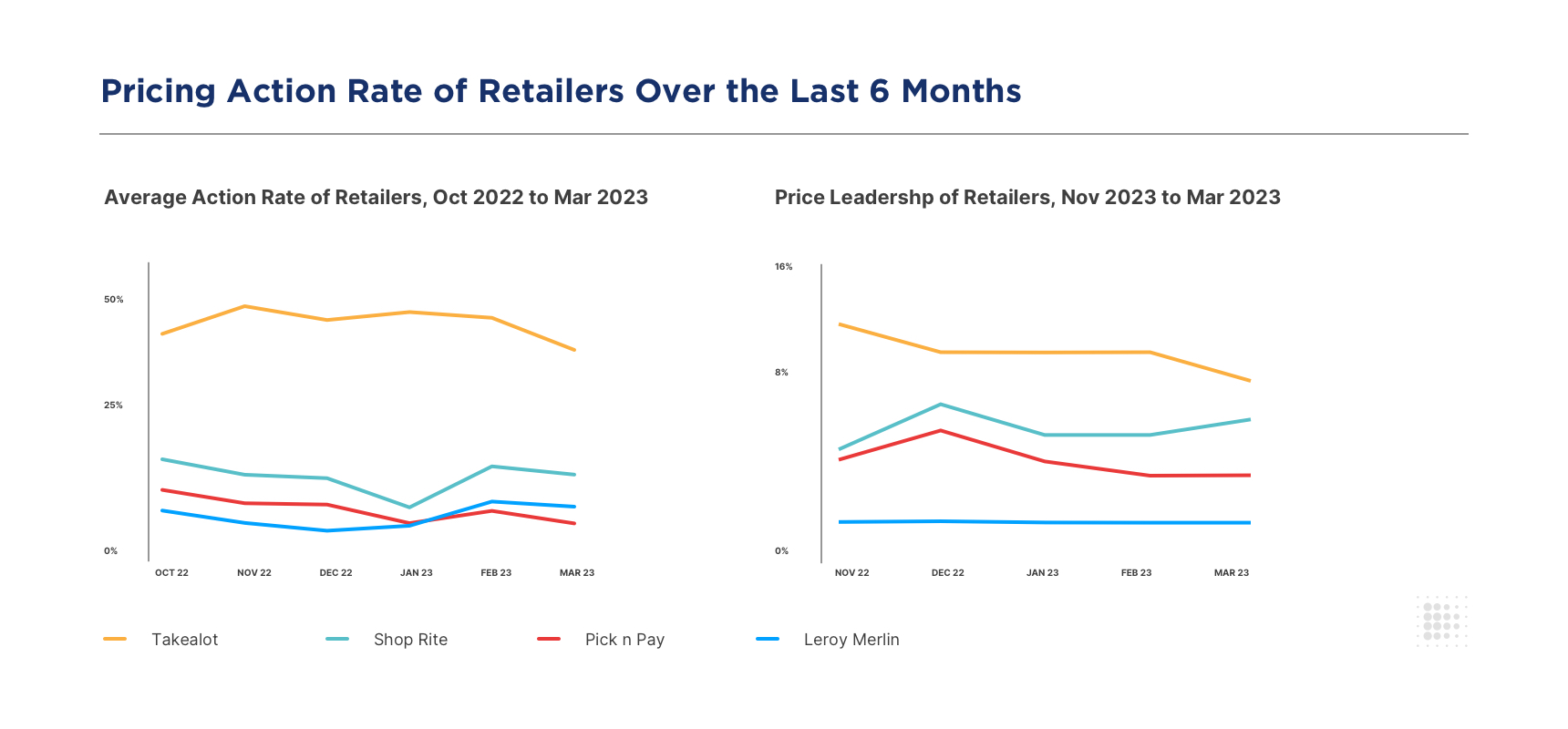

Based on the chart above, over the last 6 months, it is clear that Takealot has maintained its price leadership throughout the period, driven by consistently aggressive action rates on price improvement opportunities.

Certain nuanced trends do emerge when month-on-month variances are observed on both action rates and price leadership rates across the analyzed retailers. For example, Takealot’s actions rates have been marginally declining, which has resulted in price leadership rates also declining from 14% in November 2022 to 10% in March 2023.

Also, when ShopRite started getting more active in its action rates early in 2023, we observed an uptick in its price leadership positions. Leroy Merlin’s low action rates, coupled with low magnitudes of price changes has resulted in an average of only 2% of its products being the lowest priced relative to its competitors.

Pricing and Availability of Leading Brands

In the following section, we report on the average discounts, price parity levels, and the stock availability of the top 5 brands (in terms of number of SKUs) in each of four key product categories: Bath, Food, Home, and Spirits.

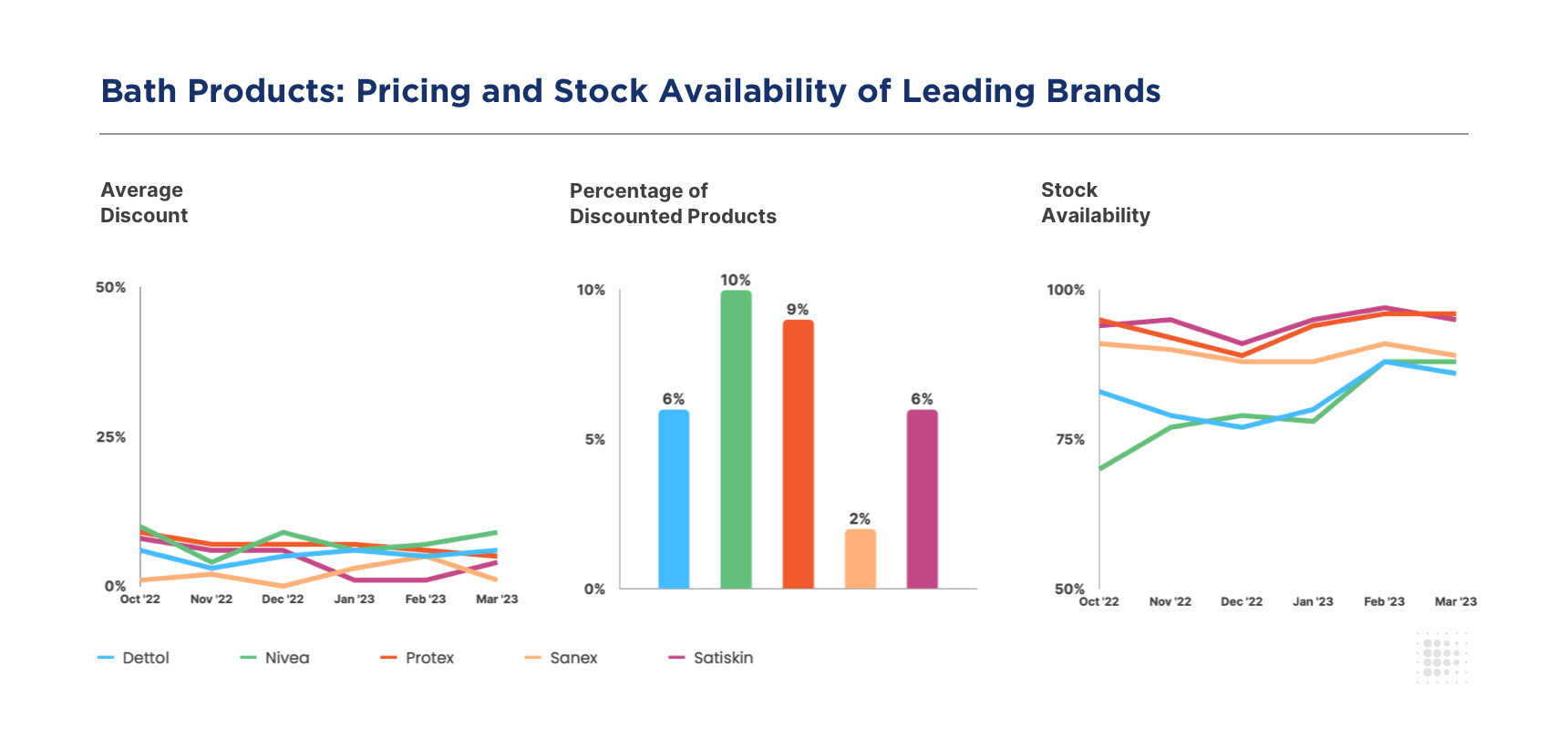

Bath

Nivea and Protex have on average been offering high discounts in the last 6 months, peaking around the holiday season in December 2022 and January 2023.

What’s more, these two brands have the highest share of their own products carrying discounts (10% and 9% respectively). Sanex has been conservative in both the average discounts offered as well as its share of discounted products.

Though Nivea has been offering attractive discounts, its stock availability has been low on average. However, it has been improving in the past few months, starting as low as 70% in October 2022 to reaching around 90% in March 2023. Dettol, too, has faced issues with its availability while showing some improvement in the recent past. All of the other leading brands in this category display healthy stock availability levels of above 90%.

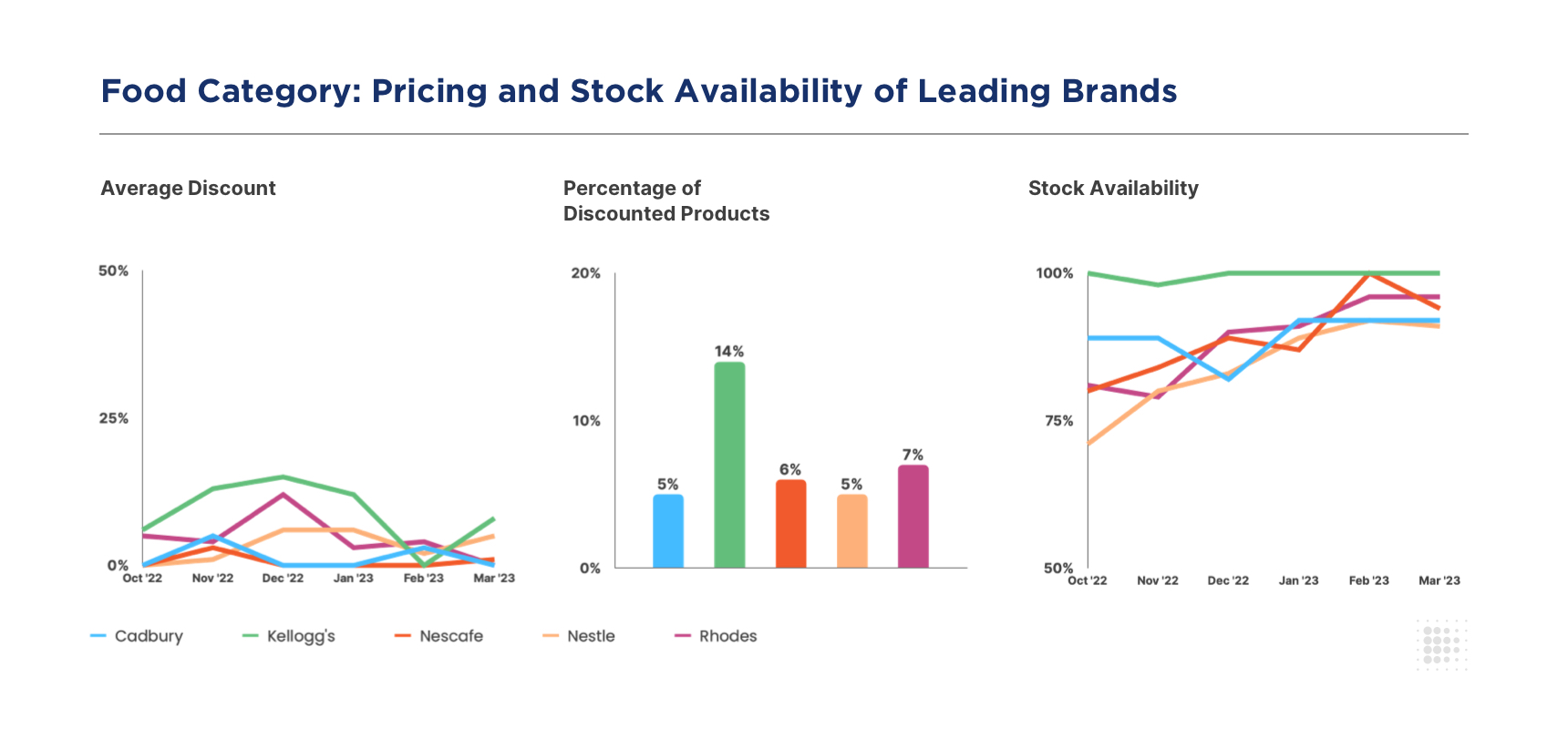

Food

Kellogg’s and Rhodes have been offering the highest discounts in the food category, especially around the holiday season. They also lead in the share of discounted products (14% and 7% respectively).

Typical to the Food category, most other leading brands have offered lesser discounts on a smaller share of their products.

In addition to offering attractive pricing, Kellogg’s seems to also have its supply chain operations in control, with almost a consistent stock availability of 100%. Most other brands struggled towards the end of 2022 and have been improving ever since. Nestle, in particular, was challenged with an availability of only 70% in October 2022, but has not improved it to 90% in March 2023.

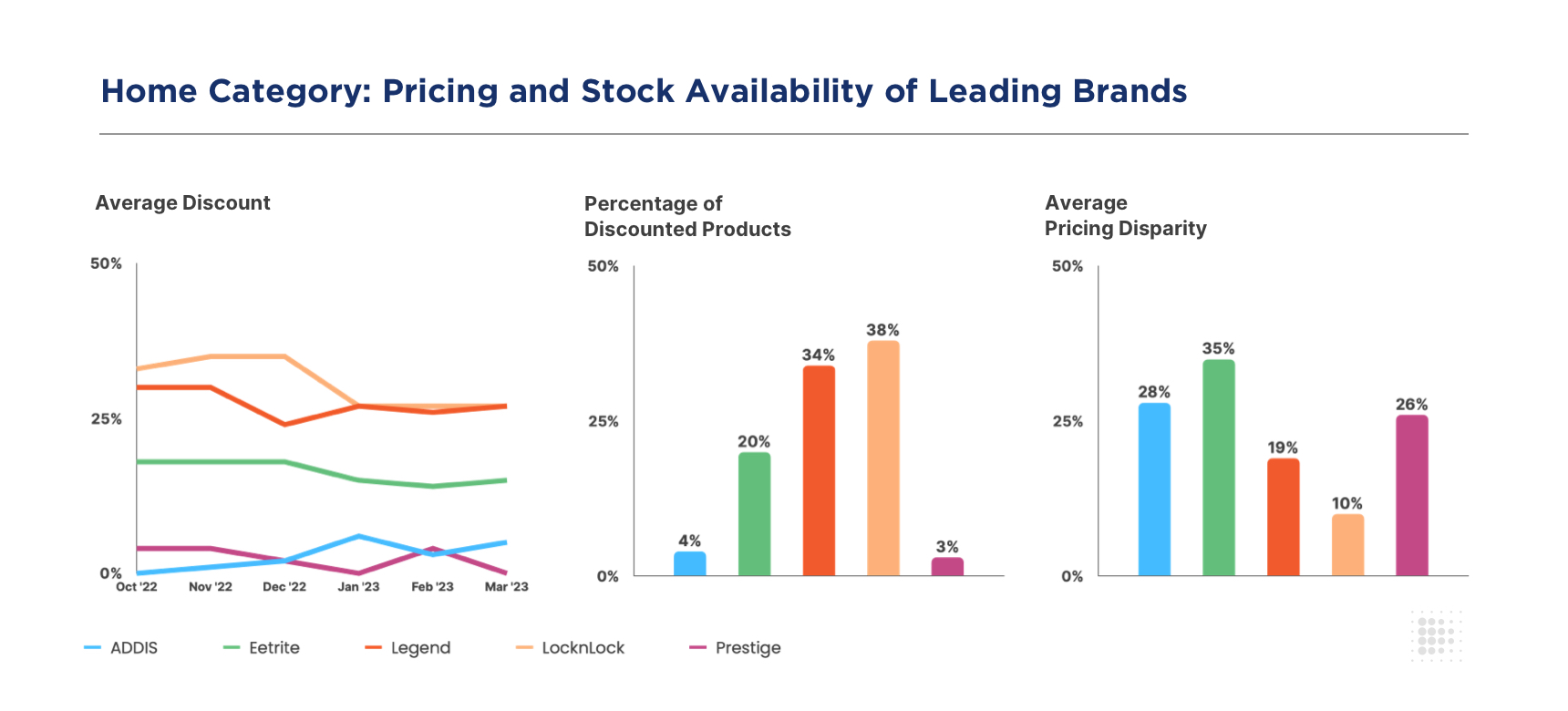

Home

The Home category displays the highest variance in discount ranges among its leading brands compared to the other categories highlighted in this report. Brands like LocknLock and Legend have been offering discounts in the range of 25% to 35% on a share of more than a third of each of their products.

On the other hand, ADDIS and Prestige have been offering discounts in the range of 0% to 5%, on a very small range of their products (<5%).

In categories like Home, maintaining a consistent brand perception among consumers is essential to boost brand value and loyalty. If there is a large disparity in the prices of the products of a brand across multiple eCommerce websites, then it negatively affects how consumers perceive the brand.

Here, the average price disparity (or variance) for LocknLock is only 10%, compared to almost 30% or more for other brands like Eetrite, Prestige, and ADDIS. Essentially, the brands discounting the most are also the ones with the lowest pricing disparity, which indicates a well thought-out, data-driven approach to eCommerce pricing and discounting – one that values both sales conversion as well as brand reputation.

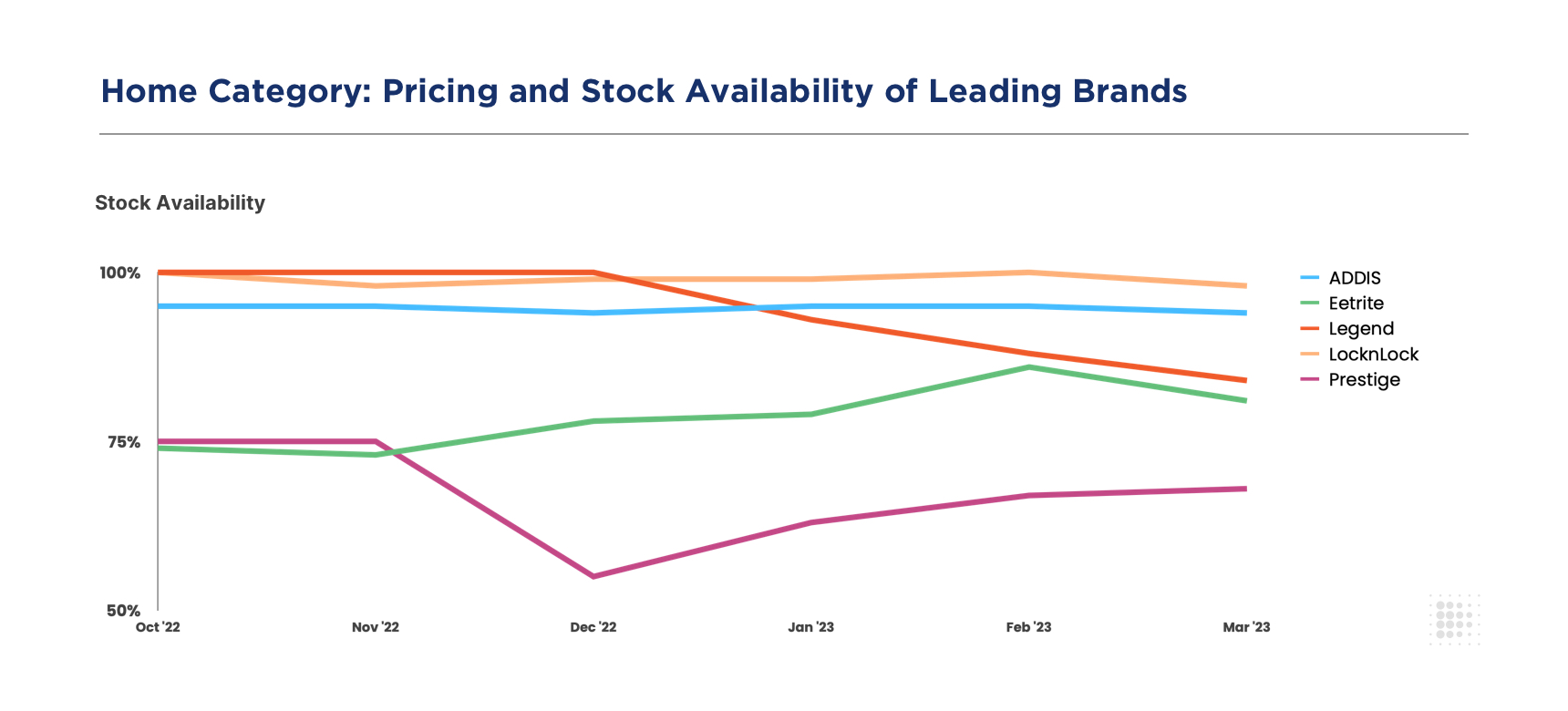

Prestige and Eetrite have been struggling with their supply chain operations, with the availability of Prestige dipping to as low as 55% in December 2022. Legend’s stock availability was strong towards the end of 2022 but has been steadily declining in 2023 so far. LocknLock and ADDIS display healthy stock availability levels of 95% and above.

Spirits

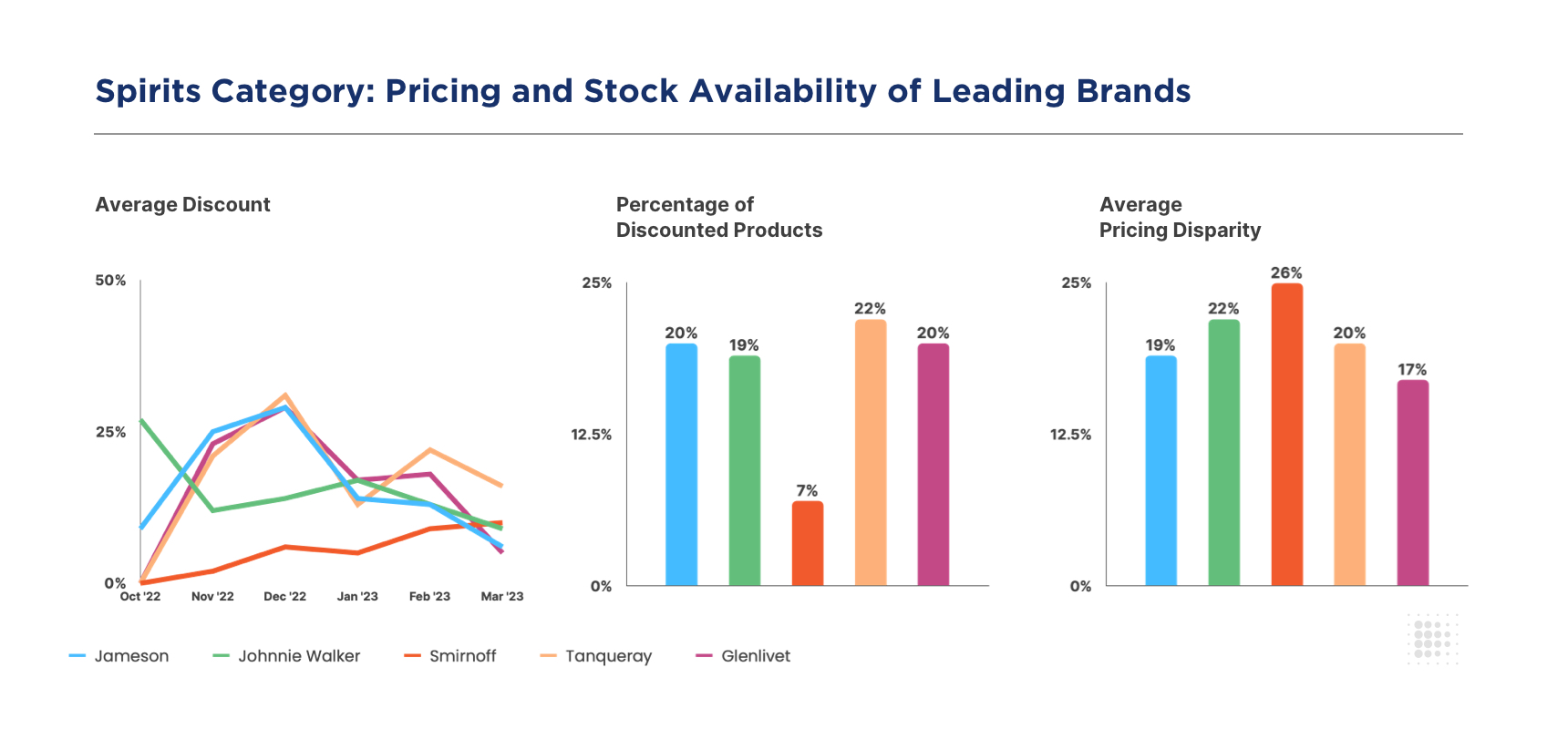

The average discounts of almost all leading Spirits brands peaked during Christmas, with Tanqueray, Jameson, and Glenlivet offering up to 30% discounts in this period.

Since then, the discounts of most brands have been oscillating within the 5% to 20% range. The percentage of discounted products for all leading brands are around 20%, with the exception of Smirnoff.

Similar to the Home category, brand perception is vital to the Spirits category as well. However, here we see almost a consistent level of pricing disparity among leading brands, varying between 18% and 25%. Brands looking to build a “premium” perception among consumers, such as Glenlivet and Tanqueray, might do well to ensure better pricing parity across their eCommerce channels.

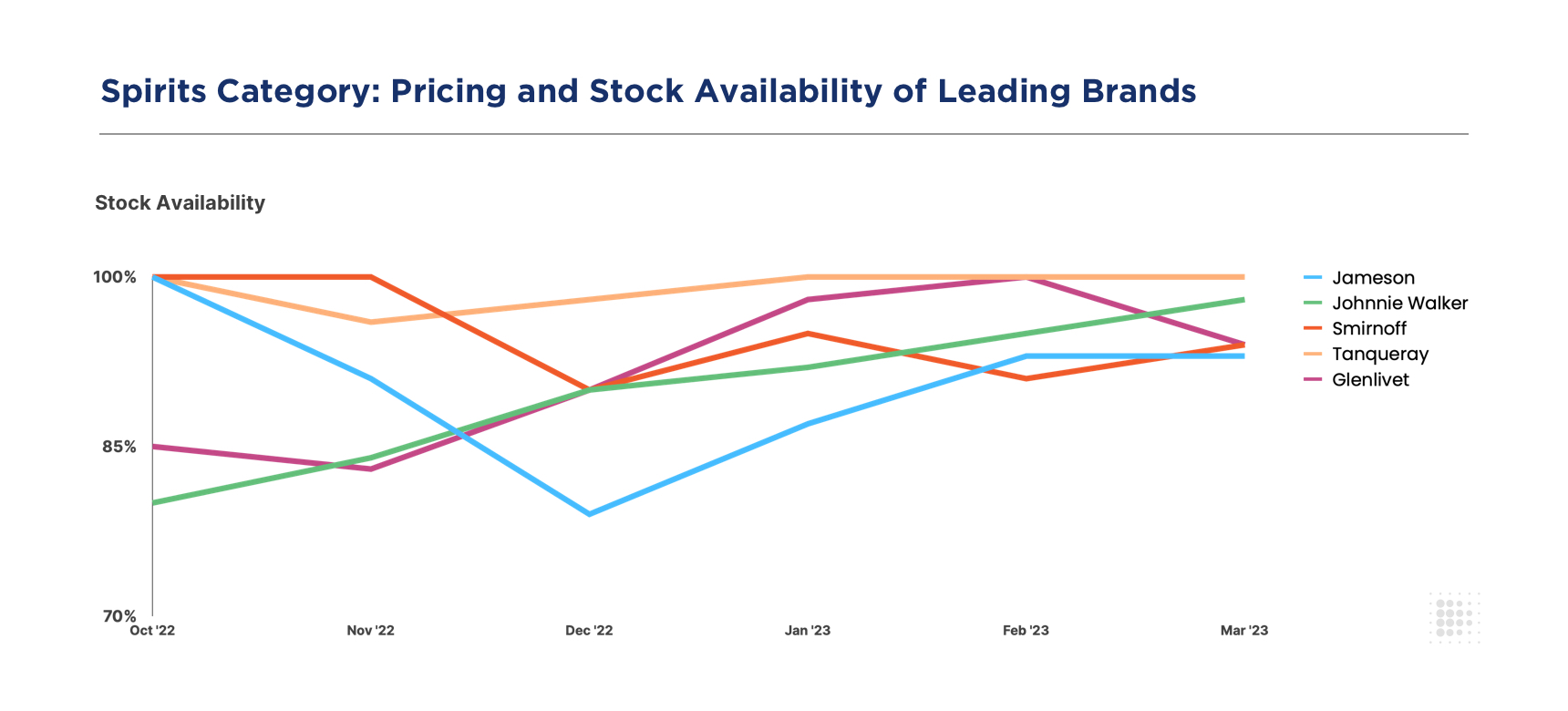

A few Spirits brands saw a dip in stock availability in December 2022, likely due to increasing demand during the Christmas season. For example, Jameson’s availability dipped to below 80% in this period. It has since improved to reach an availability level of above 90%. Johnnie Walker, too, has shown a significant improvement in its stock availability, moving from 80% in October 2022 to 95%+ in March 2023.

For more details on the state of South Africa’s eCommerce landscape as well as similar insights for other retailers and brands in the region, talk to us today!

Book a Demo

Login

For accounts configured with Google ID, use Google login on top.

For accounts using SSO Services, use the button marked "Single Sign-on".